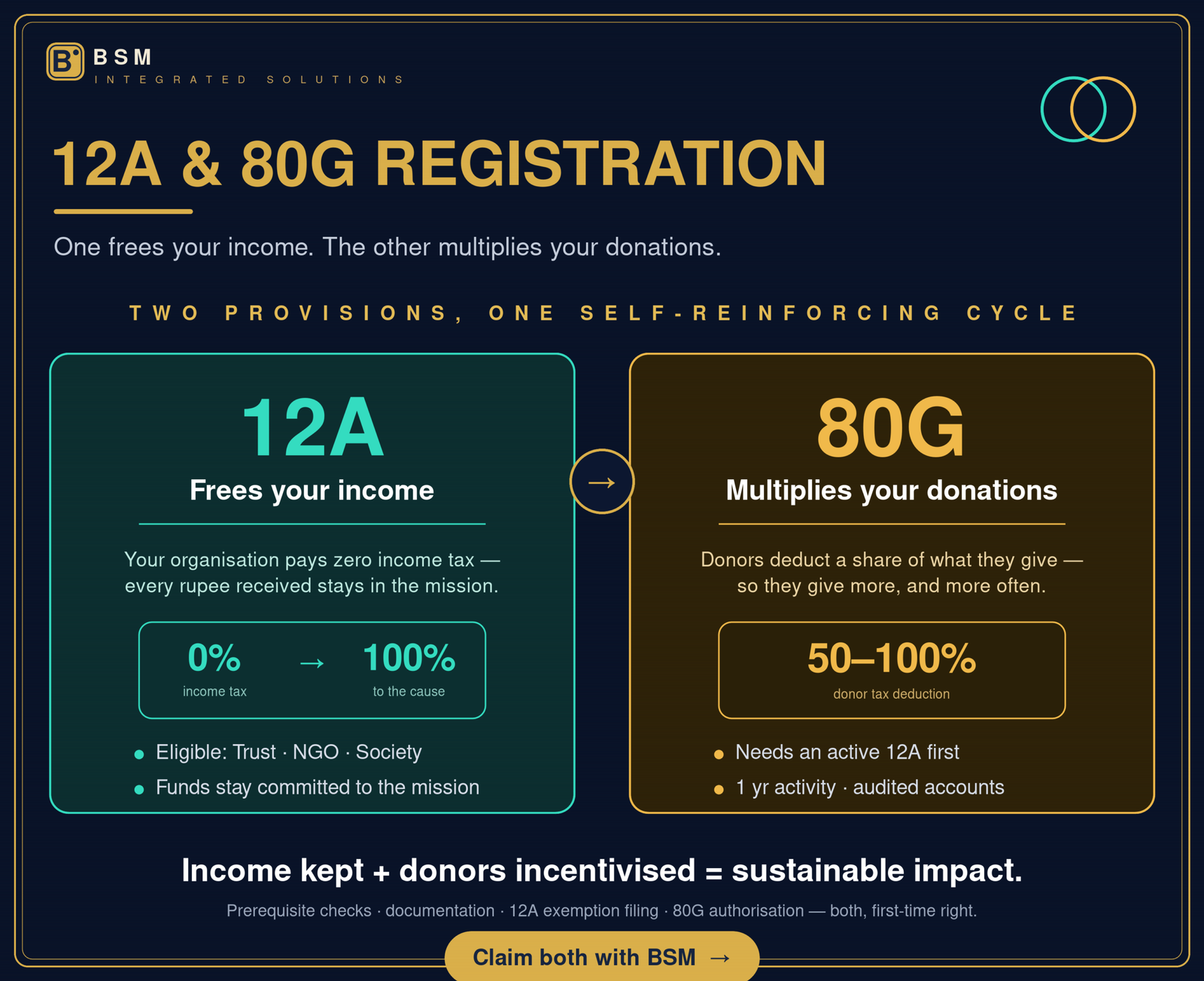

12A and 80G Registration

One Registration Frees Your Income. The Other Multiplies Your Donations.

Most non-profit organizations leave two of the most valuable tax benefits in India sitting unclaimed — not because they don’t qualify, but because they haven’t registered.

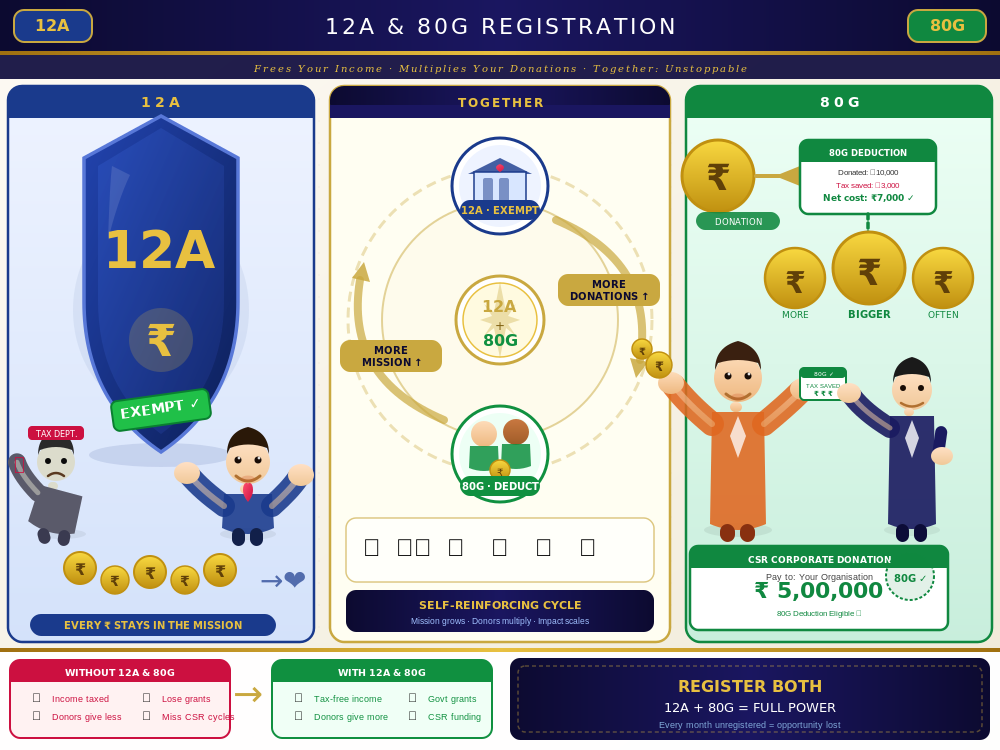

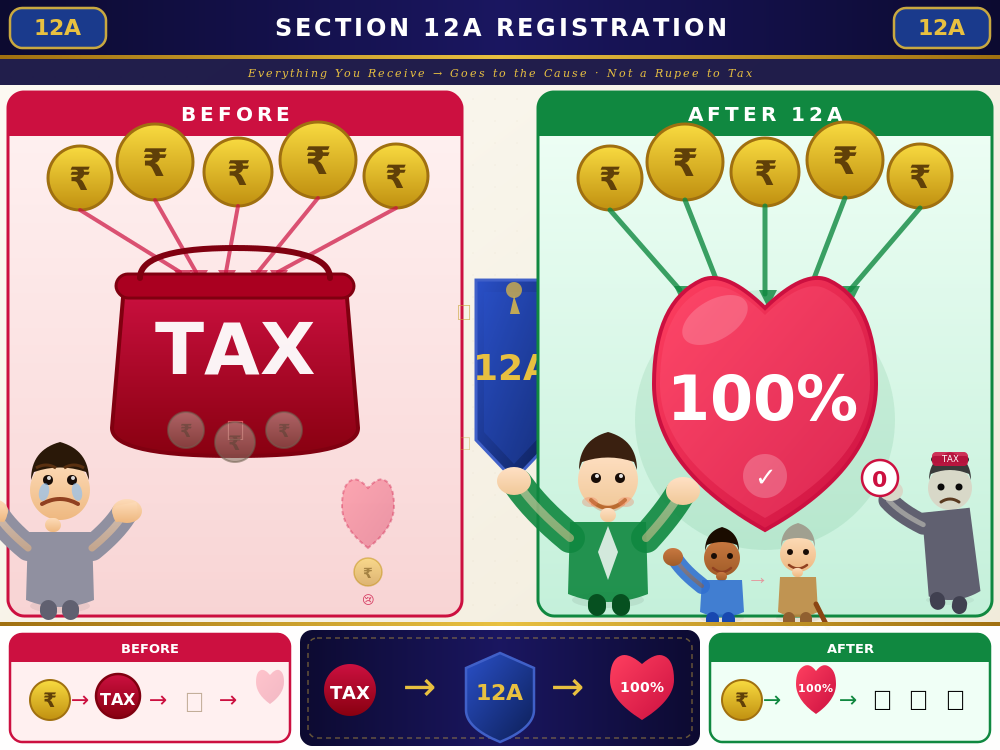

Section 12A — Everything You Receive Goes to the Cause. Not a Rupee to Tax.

Before 12A registration, a non-profit organization pays income tax on the same income it received to serve people — donations, grants, membership fees, investment returns, all taxable. After registration, that changes completely. Section 12A of the Income Tax Act grants tax exemption to charitable, religious, educational, and other specified non-profit organizations — and the exemption applies to all organizational income. Exempted organizations operate entirely tax-free, retaining 100% of received funds for charitable purposes. The organization that spent years watching a portion of every donation disappear into tax payments now keeps everything — and every rupee saved is a rupee that reaches the people the organization exists to serve.

▸ Eligibility — organizations must be a registered Trust, NGO, or Society with a documented charitable purpose.

▸ Non-distribution requirement — no profit distribution to members or founders; all funds remain committed to the stated mission.

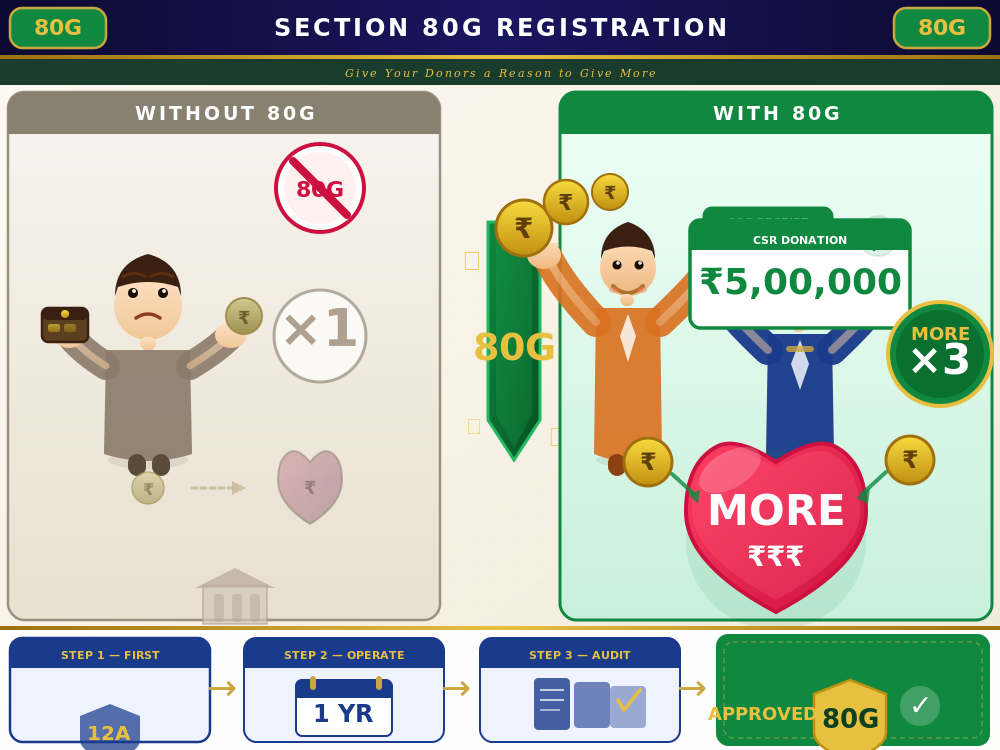

Section 80G — Give Your Donors a Reason to Give More.

The most common reason donors reduce or delay charitable contributions is not generosity — it is the absence of a tax incentive. Section 80G changes that calculation entirely. It authorizes specified non-profit organizations to receive tax-deductible donations from individuals and corporations — meaning donors can claim a deduction of 50% to 100% on contributions, directly reducing their personal or corporate tax liability. 80G registration creates a powerful incentive for increased donations while serving donor tax planning objectives. In practice: your existing donors give more. New donors — particularly corporate donors with CSR mandates and individual donors who manage their tax planning carefully — choose your organization specifically because the 80G benefit makes their contribution work harder. The donation doesn’t just go further for the cause; it goes further for the donor too.

Organizations must meet the following prerequisites before applying:

▸ Prior 12A registration — mandatory; 80G cannot be obtained without an active 12A exemption in place.

▸ Demonstrated charitable activities — a minimum of 1 year of active charitable operations, documented and verifiable.

▸ Complete financial records and compliance documentation — audited accounts and all statutory filings current and in order.

Your Organization Is Leaving Tax Benefits and Donor Confidence on the Table — Every Month You Wait.

Securing 12A and 80G registrations represents a commitment to creating sustainable charitable impact through tax-optimized operations and donor-enabled funding. Yet dual registration complexity stops many non-profit founders before they start — uncertain about eligibility criteria, confused by documentation requirements, concerned about regulatory compliance, overwhelmed by government filing procedures. And while they wait, the cost compounds: tax paid on income that should be exempt, donations not made because the 80G incentive isn’t in place, CSR funders and institutional partners who won’t engage without it. Your organization deserves tax optimization. Your mission deserves institutional credibility. Your donors deserve tax incentives. BSM becomes your 12A & 80G Registration partner, transforming dual registration complexity into official status, donor incentives, and institutional legitimacy — handled end to end. 12A exemption filing ensuring tax-free operations. 80G authorization enabling donor deductions. Prerequisite verification, documentation preparation, government filing — all of it managed correctly, the first time. That is the BSM commitment to your organizational sustainability and social impact.

Talk to BSM Today

Zero obligation · Compliance experts · Same-day response